How Much Income to Buy a House? Use an Income Calculator

How Much Income to Buy a House?

When you start looking for a home in the U.S., one question comes up almost immediately:

“Can I actually afford this house?”

You can easily check the home price, but figuring out if you can actually afford it is can be more complicated. Interest rates, property taxes, insurance, and existing debt all play a role.

Many buyers browse homes without a clear budget or rely on rough guesses.

But before you start house hunting, the most important step is understanding your affordable range.

Don’t Start with Homes — Start with Your Budget

Before looking at listings, you need to define your financial baseline.

Knowing how much home you can afford based on your income helps you:

- Avoid looking at homes outside your budget

- Avoid missing opportunities that are actually within reach

- Save time by focusing only on realistic options

Without this step, the entire home search process can become inefficient.

With Loaning.ai’s Income Calculator, you can quickly estimate the income required based on your target home price.

Instead of doing complicated calculations, you can get a clear picture of your financial range in seconds.

How to Use the Income Calculator

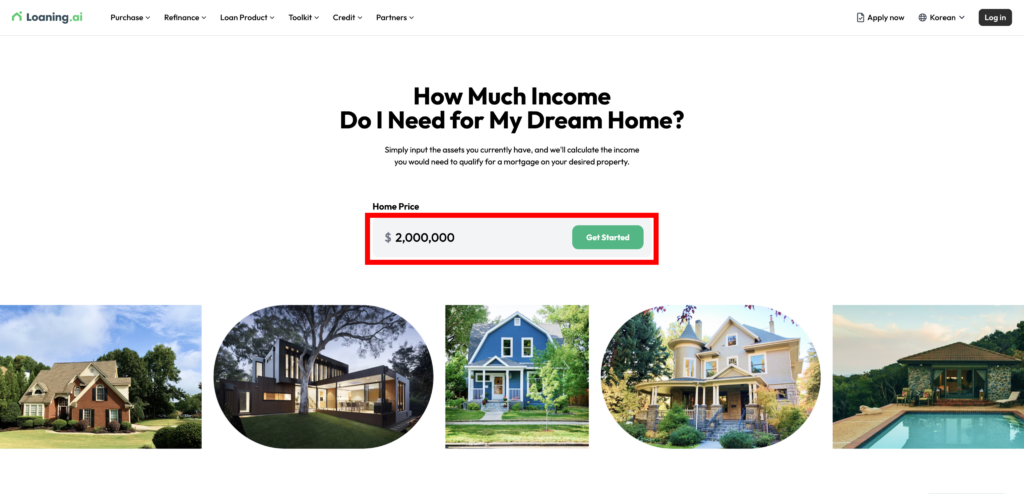

1. Enter Your Target Home Price

Start by entering the price of the home you’re considering. If you’re unsure, you can begin with an estimated price range.

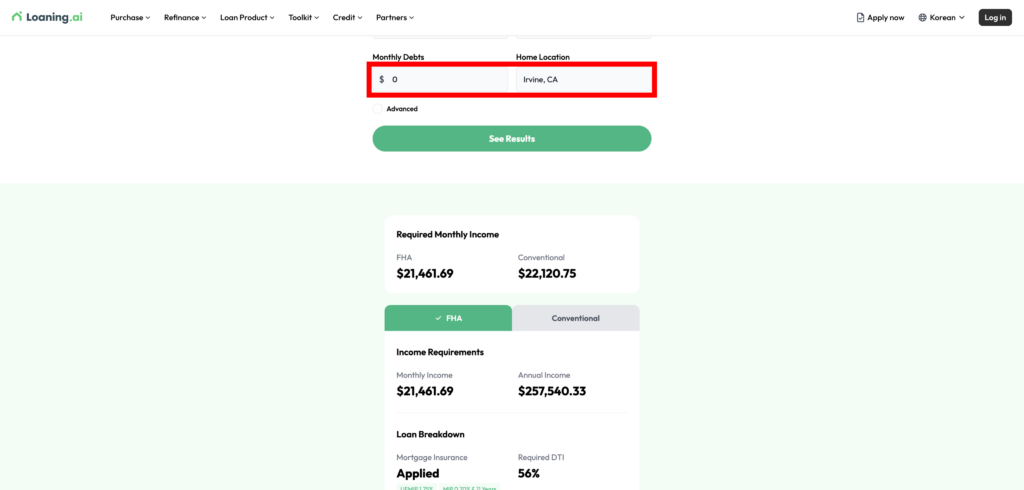

2. Add Location and Current Debt

You can also input your location and existing monthly debt.

This step is optional, but highly recommended because:

- Loan limits vary by location

- Your debt affects how much you can borrow

Adding this information gives you a more realistic result.

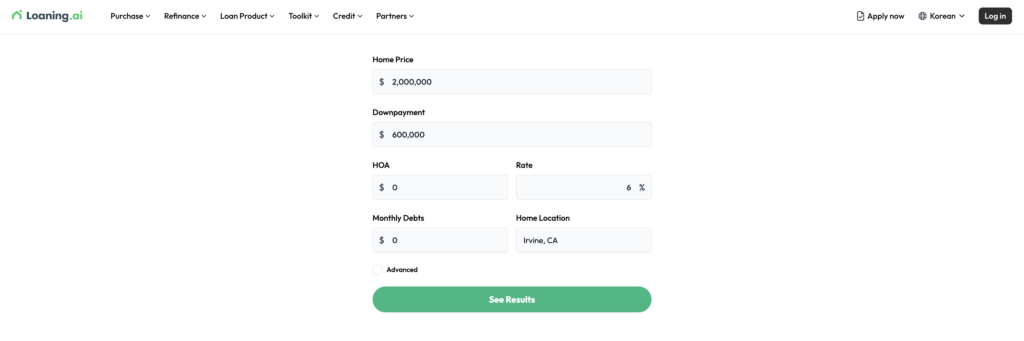

You can also scroll up to adjust:

- Down payment

- Interest rate

- HOA fees

The more details you enter, the more accurate your estimate will be.

3. Review Your Required Income

After entering your information, click “See Results.”

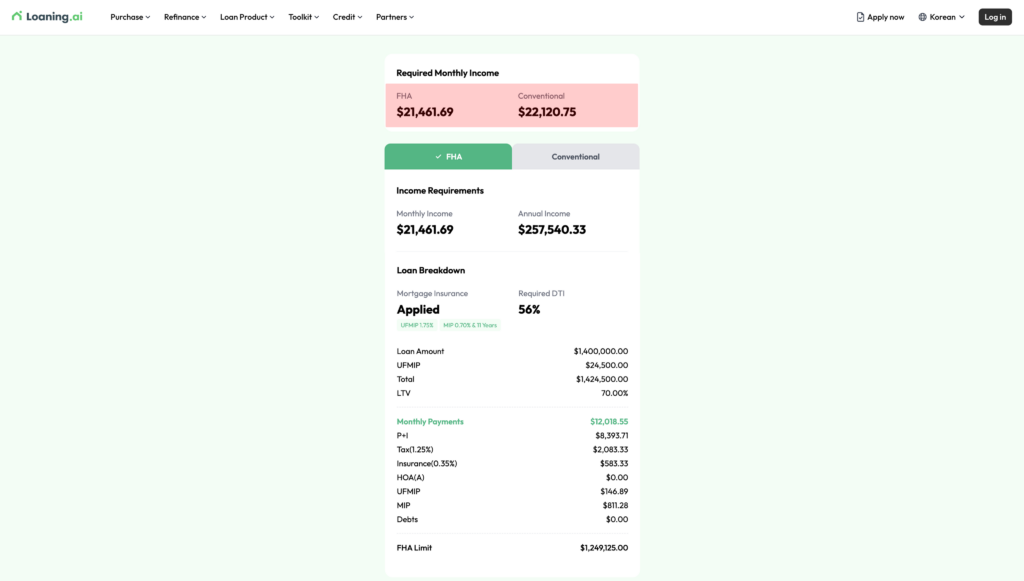

The calculator will show:

- Required monthly income

- Estimated annual income

- Monthly payment

- DTI ratio

It also compares results between FHA and Conventional loans, helping you understand how different loan types affect your required income.

DTI (Debt-to-Income Ratio) shows how much of your monthly income goes toward debt payments.

A higher DTI means:

- Lower chances of loan approval

- Stricter lending conditions

That’s why it’s one of the most important metrics to check before buying a home.

Another feature is that you can view loan limits based on location.

Since loan limits vary by area, this helps you determine:

- If you may need to consider other options like jumbo loans

- Whether your target home price falls within conforming loan limits

Start with Your Numbers First

Instead of starting with homes, start with your numbers.

Understanding how much income to buy a house helps you:

- Set a realistic budget

- Make better decisions

- Avoid unnecessary stress during the buying process