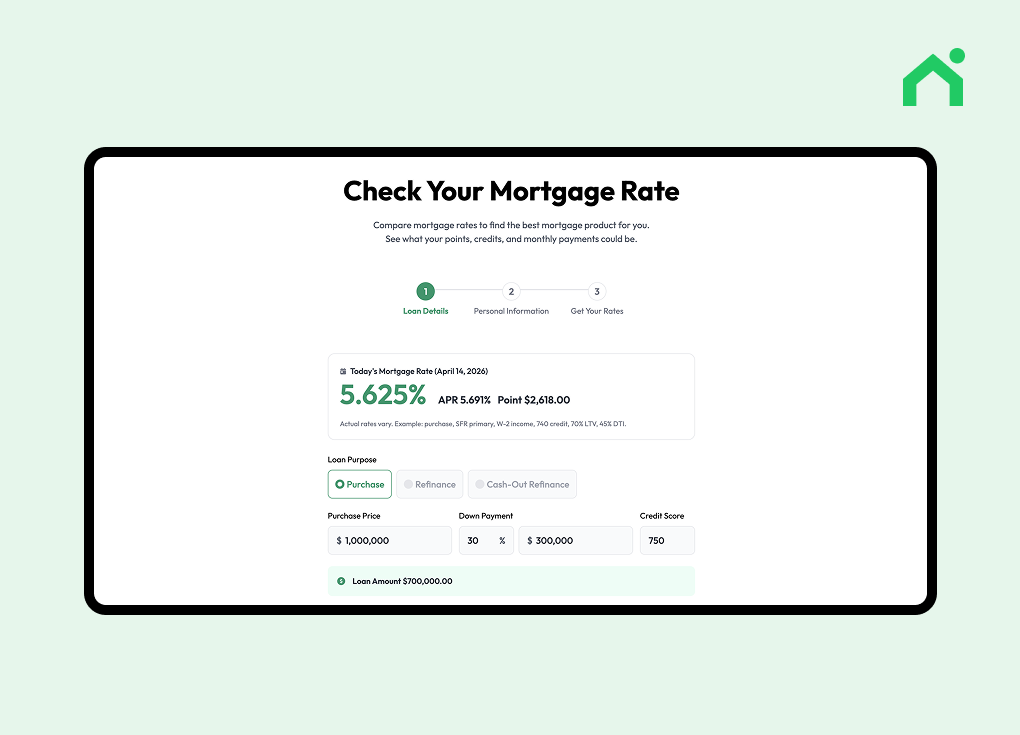

Mortgage Rate Calculator: Estimate Your Monthly Payment

In the previous articles, we first defined a realistic budget based on how much home you can afford and the loan limits in your area.

Now, the next step is to understand what kind of loan terms you can actually get within that budget.

Even if two homes are priced the same, your monthly payment can vary significantly depending on your interest rate, credit score, and down payment.

That’s why before seriously house hunting, it’s important to use a mortgage rate calculator to understand your potential rate and monthly payment based on your personal profile.

Why Is a Mortgage Rate Calculator Important?

The same home price does not mean the same cost.

Your results can vary depending on your financial situation:

- Higher credit scores can lead to lower interest rates

- Larger down payments can improve loan terms

- Investment properties often come with higher rates

In other words, what really matters is not just the home price, but the rate you qualify for.

What Can You Learn from a Mortgage Rate Calculator?

Using Loaning.ai’s mortgage rate calculator, you can go beyond basic estimates and see:

- Available interest rates based on your profile

- Estimated monthly payments

- Points / credits structure

- Differences between loan programs

This allows you to understand not just “how much,” but how your loan is structured.

How to Use a Mortgage Rate Calculator

One key advantage of this tool is that it doesn’t just ask for a loan amount.

It allows you to customize your profile in detail, including residency status, income type, and property usage.

You can also see how changing these inputs affects your rate in real time.

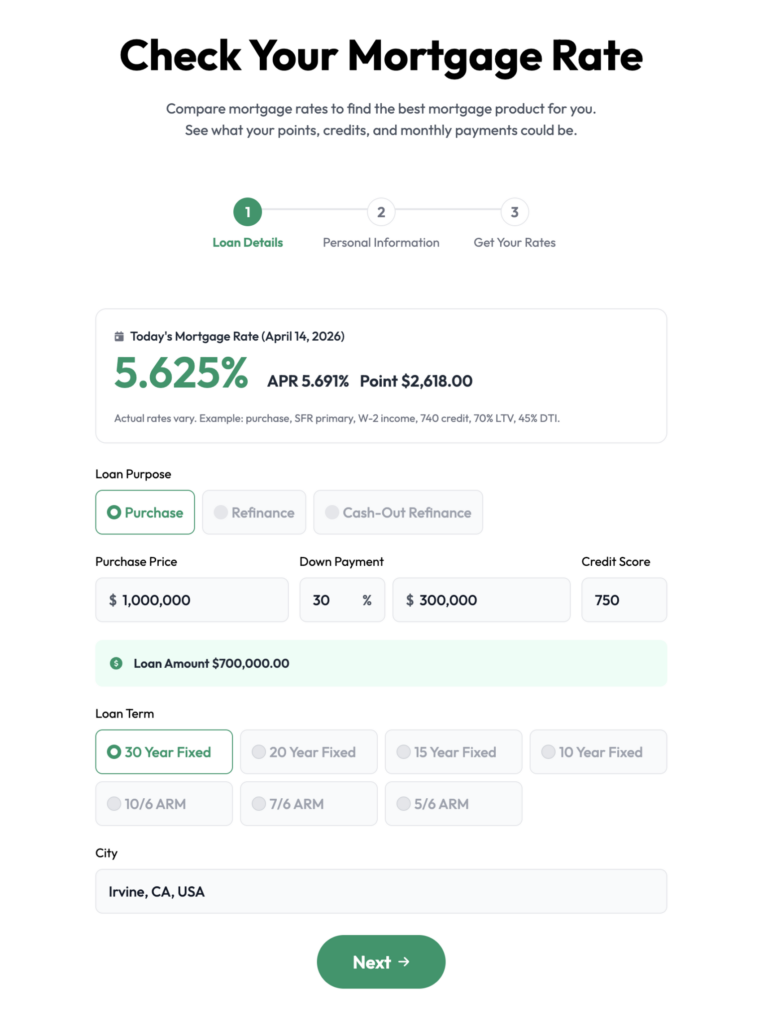

1. Enter Basic Loan Information

Start by entering your basic home and loan details.

Let’s use an example:

- Location: Irvine, CA

- Home Price: $1,000,000

- Down Payment: 30%

- Credit Score: 750

- Loan Term: 30-Year Fixed

The key point here is the baseline for each input.

- A higher down payment generally leads to better loan terms, so we set it at 30%.

- Credit score has a direct impact on your interest rate, so we used 750, which is typically considered strong enough to qualify for favorable rates.

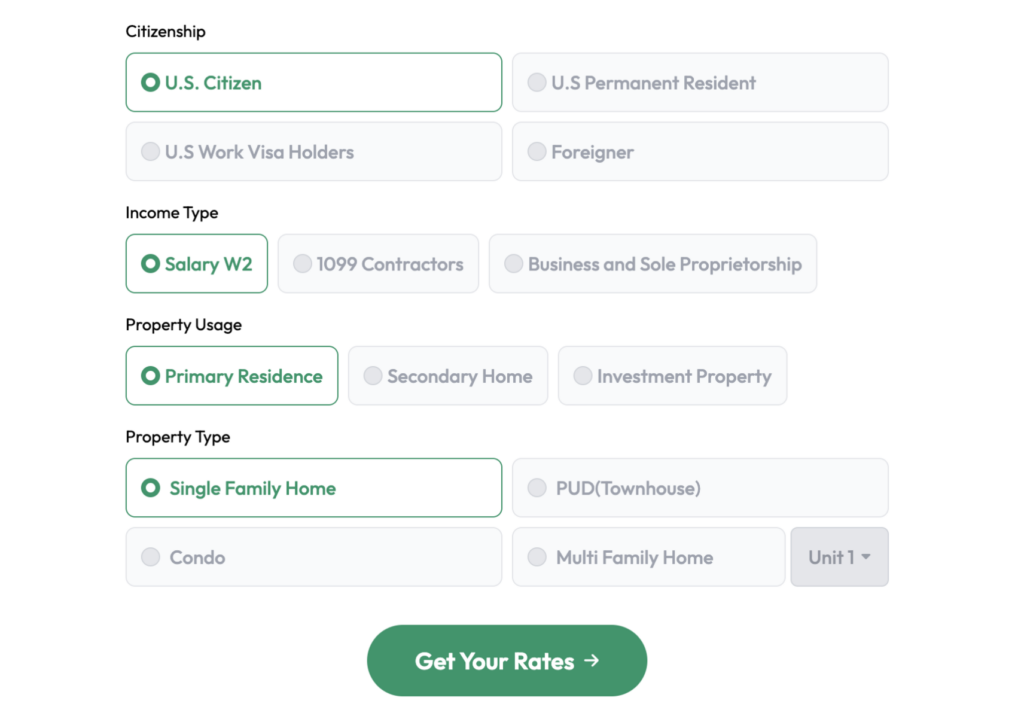

2. Set Your Personal Profile

Next, you add personal factors that affect your mortgage rate:

- Residency Status: U.S.

- Citizen Income Type: Salary (W2)

- Property Use: Primary Residence

- Property Type: Single Family Home

Under these conditions, you’ll typically see standard market rates.

However, changing any of these can affect your results.

For example:

- Switching from W2 to 1099 income → May change available loan programs and rate structure

- Changing from primary residence to investment property → Usually results in higher rates and monthly payments

Each input directly impacts your loan terms.

3. Review Your Results

Once all inputs are set, you’ll see multiple rate options.

- Rate: The interest rate you qualify for

- Points / Credits: Whether you pay upfront costs to lower the rate, or receive credits instead

- Mo. Payment: The estimated monthly payment based on that rate

For example, even under the same conditions:

- At 6.875%, your monthly payment is about $4,598.50

- At 7.000%, your monthly payment is about $4,657.12

- At 7.125%, your monthly payment is about $4,716.03

As you can see, the results can vary.

In general, as the interest rate increases, the monthly payment also goes up.

This is where you need to pay close attention to Points / Credits.

For example, some options may offer a slightly lower monthly payment, but require higher upfront costs.

On the other hand, options with slightly higher rates may increase your monthly payment, but reduce your upfront cost.

So instead of using this screen to find “the lowest rate,”

you should think of it as a decision point:

Do you want to pay more upfront to lower your monthly payment,

or reduce your upfront cost and accept a slightly higher rate?

What Should You Focus On?

A mortgage rate calculator helps you compare different structures, not just rates.

You should always consider:

- Monthly payment differences

- Upfront costs (points)

- Lender credits

Ultimately, the best choice depends on your financial situation.

Why a Mortgage Rate Calculator Makes Decision-Making Easier

Using a mortgage rate calculator allows you to see how your personal conditions translate into real numbers.

Instead of guessing, you can clearly understand:

- What rate you qualify for

- How much you’ll pay monthly

- How different choices affect your total cost

Even for the same home price, the total cost can vary significantly depending on your decisions.

That’s why it’s important to understand your loan structure before you start looking at homes.

Check Your Mortgage Rate First to Make Better Decisions

Using a mortgage calculator, you can estimate what interest rate and monthly payment you may qualify for based on your own financial profile.

It’s not just about the home price. What really matters is understanding how factors like your credit score and down payment affect your rate and overall monthly cost.

Even for the same home price, the total amount you’ll actually pay can vary significantly depending on your loan conditions.

That’s why it’s important to understand your rate and cost structure first—before you start seriously looking at homes.