Types of Mortgage Loans: Conforming, FHA, Jumbo Explained

When you start planning to buy a home in the U.S., one of the first challenges you’ll face is understanding mortgages.

At first glance, many options may seem similar—but terms like Conforming, FHA, and Jumbo can feel unfamiliar and confusing.

Because of this, many people start by asking, “Which loan is better?”

But in reality, the more important question is: Which mortgage fits my situation?

This guide breaks down common types of mortgage loans into a simple structure, so you can quickly understand your options and find the right fit.

Types of Mortgage Loans: How They Are Structured

In the U.S., mortgage loans are not one-size-fits-all.

They are generally categorized based on three key factors:

- Income documentation

- Loan amount

- Property purpose

Depending on these factors, the structure of the loan—and your available options—can vary significantly.

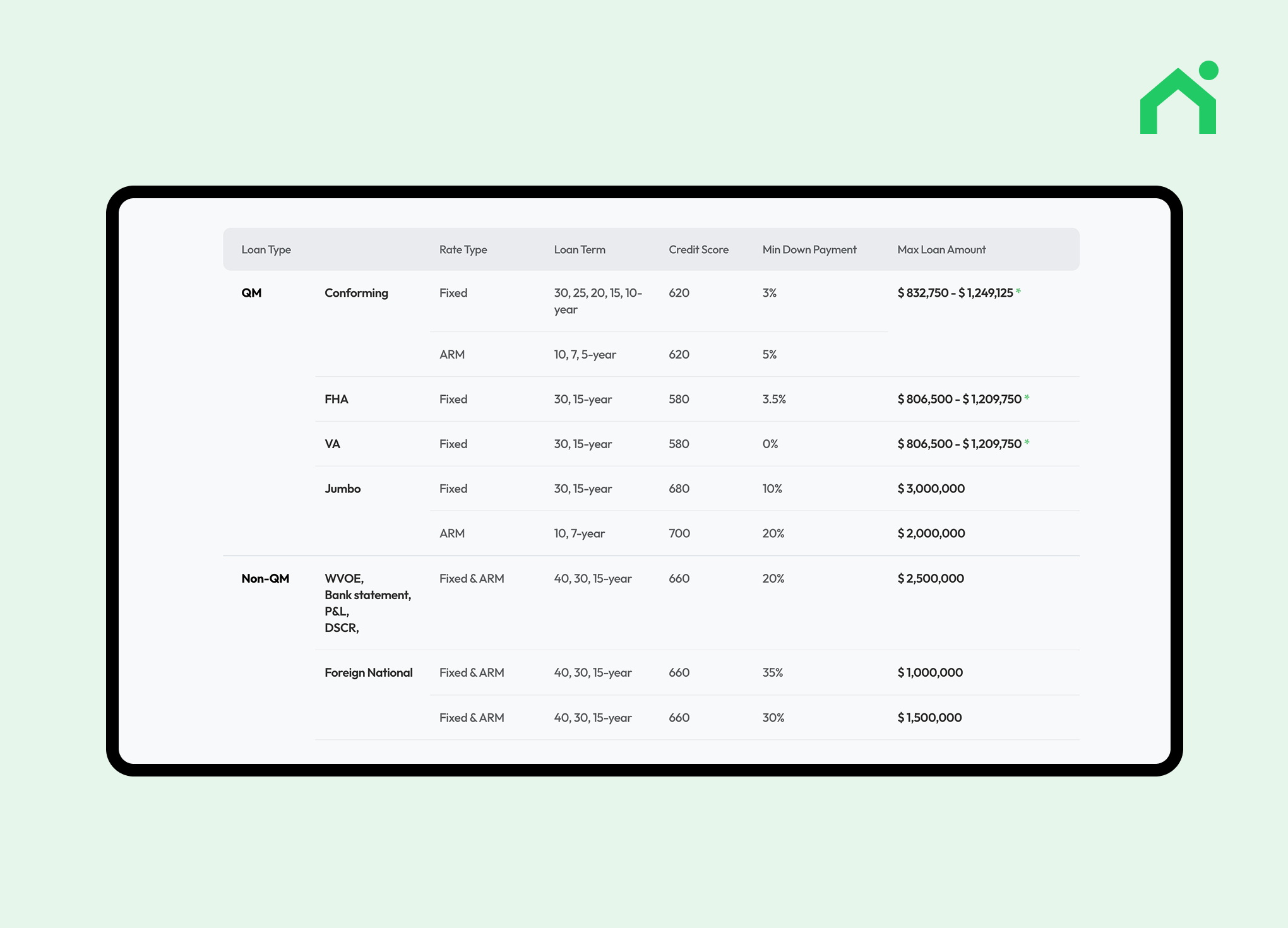

1. Full Doc Loans – The Most Common Type

This is the most widely used category, especially for W-2 employees.

- Conventional Conforming

- Conventional High Balance

- Conventional Jumbo

- FHA

- Requires standard income documents (W-2, pay stubs)

- Most stable underwriting process

- Typically offers lower interest rates

Loan types such as Conforming, High Balance, and Jumbo are determined by whether the loan amount exceeds regional conforming loan limits.

When FHA Loans Are Beneficial

- Credit score around 580+

- Minimum down payment as low as 3.5%

- Commonly used by first-time homebuyers

2. Alt Doc Loans – For Flexible Income Documentation

These loans are designed for borrowers whose taxable income may not fully reflect their actual earnings, such as self-employed individuals or freelancers.

- VOE Only

- P&L Only

- Uses alternative documentation instead of tax returns

- More flexible approval criteria

- Interest rates may be higher

- Bank statements

- Profit & Loss statements

- Verification of Employment (VOE)

Even if your reported income is low, lenders may consider your actual cash flow.

3. Investment Loans – For Real Estate Investors

These loans evaluate your ability to repay based on property income rather than personal income.

- DSCR Loan

- Based on rental income

- No personal income verification required

- Designed for investment properties

DSCR is used to evaluate loan repayment ability based on the property’s rental income, not personal income.

- DSCR = Rental Income ÷ Loan Payment

- A DSCR of 1.0 or higher means the property can cover its debt

- A key metric for investment mortgage approval

Compare Types of Mortgage Loans at a Glance

Use the guide below to quickly identify which loan type may fit your situation:

Self-employed or freelancers → VOE / P&L

Real estate investors → DSCR

| Loan Type | Income Documentation | Min Credit Score | Max LTV |

|---|---|---|---|

| Conforming (Fixed) | W-2 / Paystub | 620 | 97% |

| High Balance | W-2 / Paystub | 620 | 95% |

| Jumbo (Fixed) | W-2 / Paystub | 680 | 90% |

| FHA | W-2 / Paystub | 580 | 96.5% |

| VOE Only | Employment Verification | 660 | 80% |

| P&L Only | Profit & Loss Statement | 660 | 80% |

| DSCR | Rental Income | 660 | 80% |

Find the Right Type of Mortgage Loan for You

The most important thing to understand is that types of mortgage loans are structured differently based on your financial situation.

Your eligibility depends on factors such as:

- Whether you are a W-2 employee or self-employed

- Your income documentation method

- Whether the property is for personal use or investment

Instead of starting with interest rate comparisons, it’s more effective to identify which loan types you qualify for.

Once you know your options, you can make faster and more confident decisions.

Explore all available types of mortgage loans with Loaning.ai and find the best fit for your situation.